Digital assets and reconciliation

The inherent delays involved in traditional cross-border payments are an inconvenience, and can be a barrier to progress and efficiency. What if there were a way to make it all happen in an instant?

In banking systems, the journey of a payment from one account to another goes through several stages, often invisible to the everyday consumer. This complex process involves clearing, settlement, and reconciliation to initiate, approve, and finalize payments. However, it’s often slow and cumbersome, especially in cross-border transactions with different systems and standards.

Digital asset technology offers a revolutionary leap forward, dramatically shortening the payment cycles for businesses. Read on to find out how.

What are clearing, settlement, and reconciliation?

First, let’s take a look at how regular transactions work. The process can be broken down into three essential steps: clearing, settlement, and reconciliation.

Clearing

Clearing involves confirming the details of a transaction, such as the amount to be transferred and the parties involved. This step ensures that the buyer has the funds available and the seller agrees to the sale terms.

In the traditional banking system, clearing prepares for the actual movement of money, acting as a safeguard against potential errors or fraud.

Settlement

Settlement is the actual exchange of payment. Think of it as the moment the money physically leaves one account and lands in another. It usually takes several days, depending on the transaction type and the institutions involved.

Reconciliation

Reconciliation is the post-transaction verification process. It involves checking that the amounts debited and credited are correct and that the transaction has been recorded accurately on both ends. It's similar to balancing a checkbook or cross-verifying your bank statement against your records.

This process is crucial for businesses and financial institutions to maintain accurate financial records and ensure that all transactions are accounted for properly.

How does a transaction work?

To help you understand how clearing, settlement, and reconciliation work in practice, let’s take a look at a simple example.

Imagine you're buying a coffee. You swipe your card, and in return, you get your coffee. This transaction goes through a few steps before it's considered complete for everyone involved, not just you and the coffee shop.

Clearing: This is like saying, "I want to buy this coffee." It's the process where the details of the purchase (like who's buying, what's being bought, and how much it costs) are agreed upon and prepared for the actual money movement.

Settlement: This step is where the money actually changes hands. This is when your card payment goes through. The process takes several days because it moves through various systems and checks.

Reconciliation: After the settlement, the coffee shop needs to make sure they received the right amount of money for the coffee. This step involves checking records to confirm that the payment made matches the sale's details.

The transaction is longer and more complex than it might seem—and this is just for a cup of coffee. For larger-scale B2B transactions, like paying staff in different countries or bulk ordering raw materials, the process is essentially the same but typically takes longer as more verification is required.

Bank transfers and credit card payments

Businesses typically send and receive payments via bank transfers or with credit cards.

With bank transfers, clearing and settlement can be a slow process, often taking several days to complete, especially if your transfer falls on a weekend or public holiday. Reconciliation, too, can be labor-intensive, requiring manual verification of records.

Now, you might be thinking that paying by credit card is more convenient, but that’s not necessarily the case.

Credit card payments clear quickly because they use digital systems to initiate and approve transactions. However, settlement typically takes one to three business days. Then, reconciliation involves verifying transaction records against statements, complicated further by fees, refunds, and chargebacks (refunds requested by the cardholder, often due to disputes such as not receiving an item or being charged incorrectly).

With both bank transfers and credit card payments, a transaction involves a lot of steps and can take several days. There's paperwork, verification, and waiting periods.

Fortunately, there is a better way: using blockchain-based digital assets.

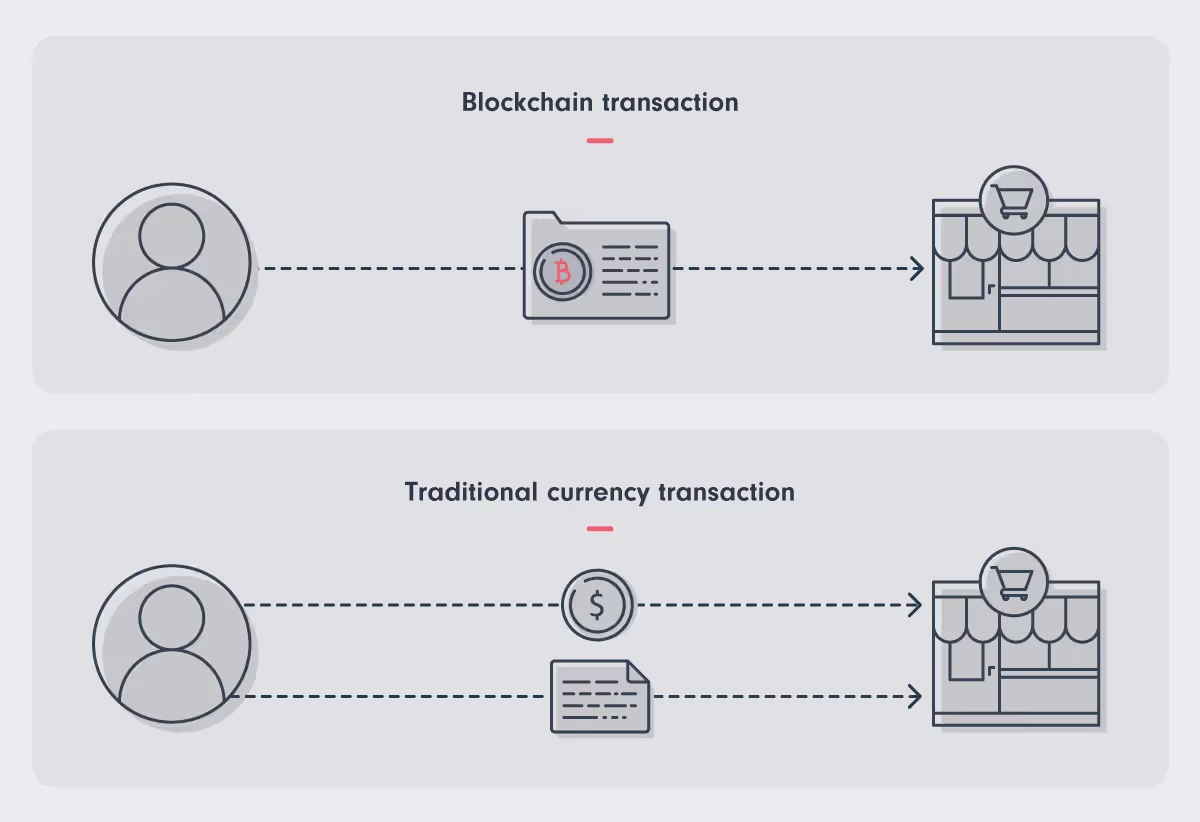

Payments on the blockchain

Blockchain technology simplifies the clearing, settlement, and reconciliation process.

In a blockchain transaction, when you transfer digital assets, the process merges the verification of the transaction (confirming it's legitimate) with the actual movement of funds. This happens in a secure and almost instantaneous manner. Once the transaction is added to the blockchain, it's confirmed and cannot be altered, ensuring both parties have clarity and certainty immediately.

Going back to our coffee shop example, imagine paying via the blockchain. You initiate a payment, directly transferring digital funds to the coffee shop's wallet. This action is immediately verified and permanently recorded on a public ledger, visible to all but unchangeable. The coffee shop sees the payment in real-time, and the deal is sealed right away.

Why is it so fast compared to traditional payments? Blockchain technology operates without a central authority. In traditional banking, a central entity like a bank confirms the transactions, whereas blockchain transactions are validated by a distributed network of computers.

The lack of a central authority boosts efficiency and reduces the potential for errors and disputes, making blockchain an attractive option for businesses.

This decentralized system is enabled by public key cryptography, a secure method of digital communication that ensures only the intended recipient can access the sent funds. This ensures blockchain transactions are not only fast, but also secure.

To learn more about how this works, consider reading up on public key cryptography, which provides the building blocks for secure, direct transfers of digital assets on the blockchain.

Benefits of digital asset payments

Here are the main advantages of digital asset payments:

- Value travels with the message: When you make a payment with digital assets, the confirmation and the transfer of value occur almost instantly. The transaction record and the actual movement of money are part of the same action.

- Settlement and reconciliation in one: Digital asset transactions combine settlement and reconciliation into a single step. There's no need for a separate, lengthy reconciliation process. The transaction is final once confirmed on the blockchain, providing clarity and certainty for both parties.

- Greater visibility and transparency: Everyone involved can see the transaction details on the blockchain, which helps with reporting, accounting, forecasting, and compliance.

- Simple international payments: Sending digital assets internationally is as easy as sending them domestically, with no need for currency exchanges or additional fees.

Digital asset payments with Fortris

Fortris enables enterprise businesses to take advantage of the speed and efficiency of blockchain payments.

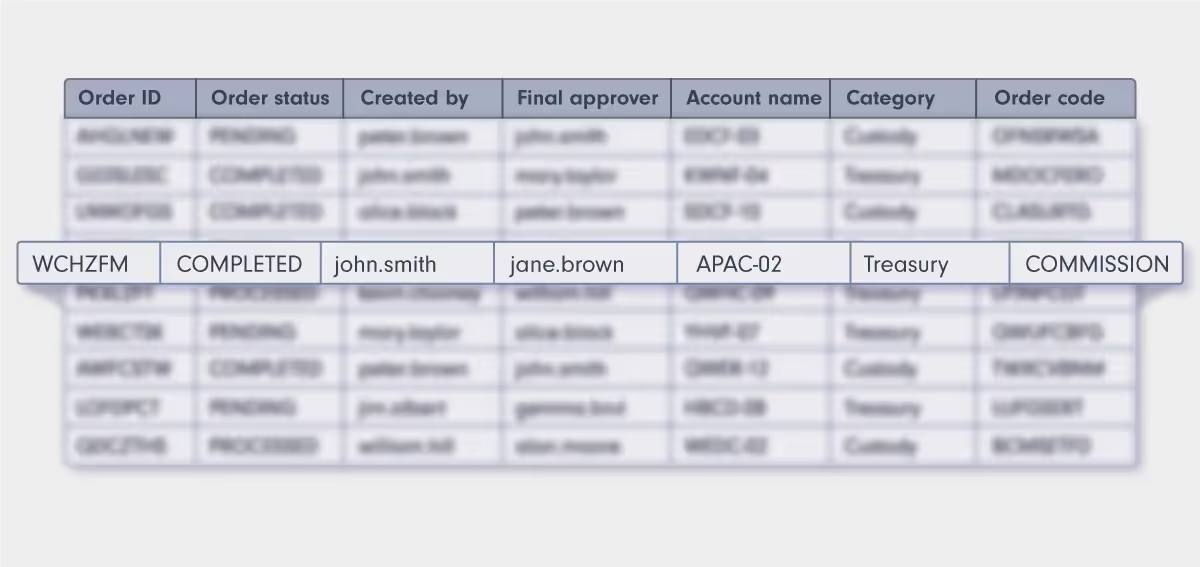

An example of a journal report for a digital asset transaction in the Fortris system

Fortris provides an off-chain record of all on-chain transactions using live data from the blockchain. It’s a bit like bank feeds in accounting software, offering side-by-side comparisons of your transaction records with imported bank data.

The transaction labeling system automatically fills in the details of each transaction, whether receiving or sending, which in turn:

- Eliminates manual efforts from the reconciliation process

- Streamlines and automates cash flow forecasting

- Simplifies the closing process

- Enables verification of all transaction records against the blockchain.

Each transaction entry in Fortris is enriched with both exclusive organization-specific data and publicly available blockchain information, providing a comprehensive view.

This makes it easier for businesses to manage transactions, especially when dealing with payments across borders or in high volumes. With Fortris, managing and reconciling payments is no longer a tedious task but a seamless part of your business operations.

To see an example of what this looks like in practice, read our article on what a Bitcoin journal report looks like in Fortris.

Fortris handles digital asset treasury operations for enterprise business.

Want to learn more? Book a demo today.

Fortris handles digital asset treasury operations for enterprise business.

Want to learn more? Book a demo today.